Required Minimum Distribution (RMD) Calculator

This calculator uses the IRS Uniform Lifetime Table (effective 2025) for RMD calculations. Enter your prior year-end balance, date of birth, and calculation year to estimate your required withdrawal. Roth IRA owners do not have RMDs during their lifetime.

Your RMD

Note: This calculator uses the IRS Uniform Lifetime Table effective January 1, 2025. The RMD age is 73 (increases to 75 in 2033). This is an educational tool only and not tax advice. Visit CalculatorUp.com for more free financial calculators.

Required Minimum Distribution

Required Minimum Distribution (RMD)

Required Minimum Distribution (RMD) is the minimum you can take out of several retirement plans annually.

It applies to 401(k) plans, traditional IRAs, SEP IRAs, SIMPLE IRAs, and similar accounts.

According to the IRS, you must make this withdrawal after you turn a particular age.

How Does It Work?

The IRS sets rules for RMDs. You cannot leave money in retirement accounts for life. The government wants you to withdraw and pay taxes on it. Each year, you must take out a portion of your balance. The amount depends on your age and account value.

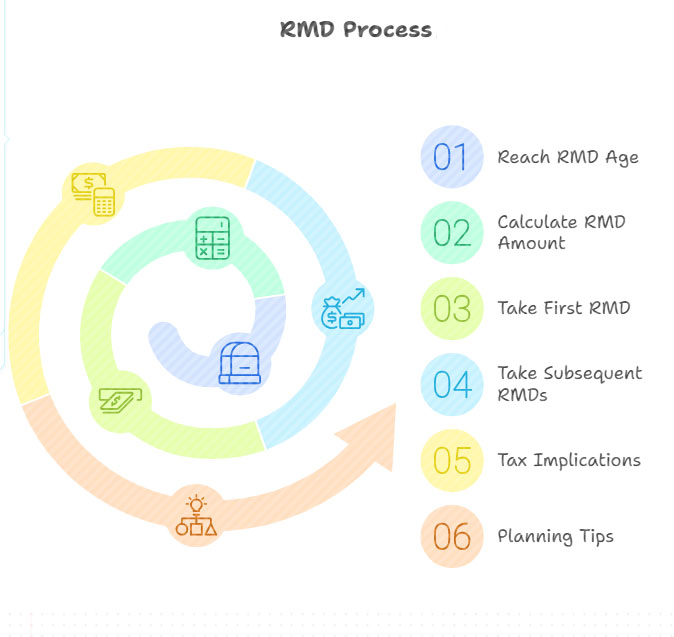

Step-by-Step Guide to Calculating Your RMD

-

Find the balance of your retirement account on December 31 of the previous year.

-

Get your life expectancy value from the IRS table.

-

Divide your account balance by that number.

-

The result is your RMD for the year.

When Do You Need to Start Taking RMDs?

You must start taking RMDs at age 73 (for most people today).

You need to take your first RMD by April 1 of the year after you turn 73. From the second year on, the deadline is December 31 each year.

How to Withdraw RMD Without Paying Extra Taxes

You cannot avoid paying taxes on RMDs. But you can reduce extra costs. You can send your RMD directly to a qualified charity.

This process is known as a Qualified Charitable Distribution (QCD). A QCD is not taxable. You can also plan withdrawals to avoid moving into a higher tax bracket.

Common Mistakes to Avoid with RMDs

-

Forgetting to take the RMD.

-

Taking less than the required amount.

-

Missing the deadline of December 31.

-

Mixing up multiple accounts and not calculating each one.

-

Ignoring tax planning for large RMDs.

RMD Rules for Traditional IRAs

Traditional IRAs require RMDs after you reach age 73. You must take them each year by December 31. The amount is based on the IRS table.

RMD Requirements for 401(k) and 403(b) Plans

If you own a 401(k) or 403(b), you must take RMDs from each account. You cannot combine them like IRAs.

Do Roth IRAs Have RMDs?

Roth IRAs do not have RMDs during the original owner's lifetime. You can leave the money in the account as long as you want. But if someone inherits your Roth IRA, they may need to take RMDs.

Inherited IRA and RMD: What Beneficiaries Should Know

If you inherit an IRA, the rules are different. Beneficiaries generally have to withdraw all funds within a 10-year period. Some may qualify for lifetime payouts. Spouses have special options, such as rolling it into their own IRA.

RMD for Multiple Retirement Accounts: How to Handle Them

If you have multiple IRAs, you can calculate the total RMD for all and withdraw it from one or more accounts.

How to Minimize Taxes with Smart RMD Planning

You can lower taxes by carefully planning RMD withdrawals. Spread withdrawals across the year to avoid a large tax bill. Consider taking smaller amounts monthly or quarterly. Use tax-advantaged strategies like Roth conversions before RMD age.

RMD Strategies for Retirees in Their 70s and Beyond

Retirees should make sure that their RMDs are enough to cover their expenses. Instead of saving money, use RMDs to pay for living costs. Plan your withdrawals so you don't have to pay more taxes. Check your tax situation every year and change your withdrawals as needed.

How to Use Charitable Donations to Meet Your RMD (QCD Strategy)

You can give your RMD directly to a qualified charity. It is a Qualified Charitable Distribution (QCD). A QCD doesn't have to pay taxes and contributes to your RMD. It lowers your taxable income while helping a good cause.

2025-09-05 21:38:41

John Carter